|

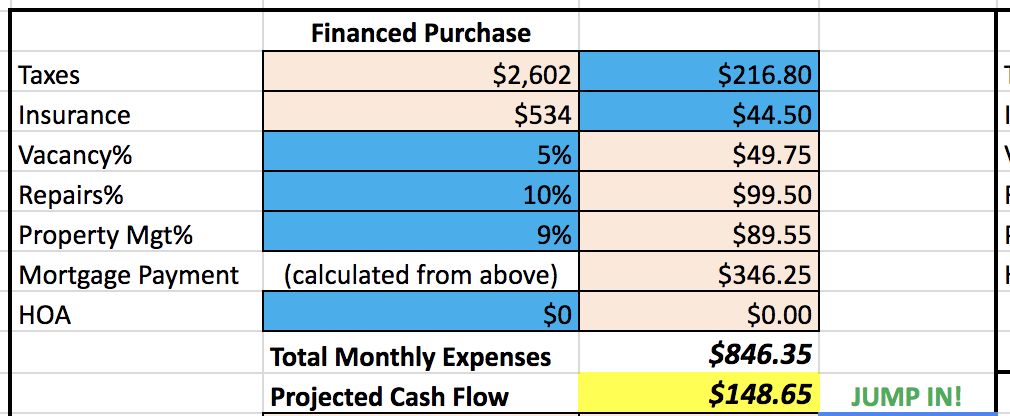

Cha Ching! My Second Property is officially a performing asset. Today, I got my first rental payment. With my tenant's lease starting on May 22, I received pro-rated rent for the remainder of May. That adds up to the grand total amount of $331.60.  I'll get my first full rental payment on June 1st for the amount of $995. Below is what I should expect my monthly finances to look like on this property:  Thanks to fellow Indy investor Alex for this spreadsheet! As you can see, my expected monthly cash flow is $148.65 per month. That's after I set aside money for repairs ($99.50) and vacancy ($49.75) and keep them in my reserves. ALWAYS, ALWAYS, ALWAYS factor in vacancy and repairs in your numbers for future expenses!!!

Now, what do I say next... Well, I'm really not sure. WOW. Another property in the portfolio. Another property in Indianapolis. 2,000+ miles away from my home in the San Francisco Bay Area. The property is officially rented and cash flowing! Crazy how I've now been involved in 3 real estate transactions (2 purchased + 1 sale) over the past year and a half. This all has really developed so fast. Luckily, I was put through an experience early on that greatly contributed to my growth in the real estate world. I adjusted my strategy on this property and I'm confident in better long-term stability and returns on this one. Jumping Into a higher priced property in a better neighborhood is critical for my investing goals and I'll continue this strategy moving forward. Takeaways -It's amazing to reflect on the whole process from initial analysis, to offering, to negotiation, to marketing, to property management. There's a lot that goes into investing in out-of-state real estate, but it's all worth it once you get that first rent check. -Just because you get that first rent check, doesn't mean everything is going to be great and dandy from there on out. Challenges will pop up, unexpected expenses will be thrown at you, but remember, buy and hold investing is a LONG-TERM play. What's next? Acquiring My Third Property, OF COURSE! Stay Tuned! GOT A QUESTION? Email, Call, Text, or Slide me a DM HERE! Or leave a comment below. I'd love to chat! Happy Investing and Best of Luck! -Tyler

0 Comments

Ho. Lee. Crap. I'll just start by saying, you really can't expect IMMEDIATE results. And that doesn't just apply to real estate investing, or marketing a property for rent...that just applies to life in general. There's your words of wisdom for the day :) But, back to getting my property rented.  So, at the end of March, I took a little risk, and listed my property at $1,050 in hopes of getting $50 more per month than I was anticipating. Long story short, that experiment didn't work out. Yes, I got a couple applicants, but they ended up not qualifying to rent the place according to my Property Manager's standards. At one point, I had another strong lead, but they had a dog...and going into this whole landlord business, I've always been opposed to having pets in my properties. I have nothing against animals, I just fear the worst sometimes and foresee urine stained carpets and wrecked walls. I'd like to avoid that and protect my investments. A couple weeks go by, and I decided to drop the rent from $1,050 to $995 (my property manager felt keeping it under $1,000 would attract more renters). Kinda sucked that my decision to start with a higher rent didn't work out...but that's life. A couple MORE weeks go by. OK, now things are getting a little worrisome. Doubt creeps into your head. It definitely crept into mine. Here we go again...should I have even bought this property in the first place? Is real estate really a great investment?? I ran through all the scenarios and plugged lower rents into my spreadsheets. What would my return be on the property if rented at $850? What about $800? Worst case scenario would be $750, right? RIGHT?? Remember, I live in the San Francisco Bay Area where properties literally go on the market in the morning and are rented by the evening. I've been trained to expect a highly competitive rental market. Deep breath. Indianapolis is not San Francisco. Today, April 27th. I GOT A SIGNED LEASE! It took some time. It took a lot of personal patience. But, at the end of the day. I got a signed lease. There's still a slight bummer...the tenants aren't moving in until May 22nd...so there's still some time until I start getting payments. I'll end up having to pay my first mortgage payment on May 1st without a renter, but that's why you have reserves. Bottom line: this property is very close to becoming a performing asset. And at the end of the day, that's all that matters. Takeaways -Listing your rent at the appropriate price is very important. I'm not upset for trying to list a little higher than expected...it ultimately cost me a couple weeks...but I felt it was worth the risk. However, if you are tight for cash and need the income immediately, I wouldn't recommend taking the risk. Consult with your property manager. They're the experts. -Patience! If you live in a competitive rental market and you invest in the midwest/out-of-state, you must recognize properties sit on the market longer. It's just the nature of it. Have reserves in place to cover vacancy and practice patience. Next up: time to start getting cash flow! -Tyler Property management is in place. Things are looking good. I got lucky with this property because it's in great shape. Really, all that needed to be done was general cleaning ($250) and I had to replace a broken window in the garage ($136). There are a couple additional minor repairs I'll take care of later, but they are not a major priority right now. I need to get this thing on the market ASAP and avoid a long vacancy. My first mortgage payment is due in a month! First thing first: get a professional photographer in there. My new property management company knows how to get a house rented. And first impressions are key to potential renters. High quality photos are a basic marketing tool you need to understand.

As you can see, the property does need some interior updating, but I'm not worrying about that right now. It's clean and has great bones. Next up: setting the rent price. If you recall, the previous tenant was paying $1,000 a month. So when I decided to acquire this property, I ran my numbers based on that rate. However, there was indication from local research and data that I could get a little more. So, I'm taking a little chance. I'm setting rent at $1,050. An extra $50 a month would be great and I feel it's smart to take this risk. If there's no traction in a week, no interest or applications, then I'll re-assess.  Takeaways -Getting your property cleaned up and ready to rent ASAP is key. Vacancy is one of the largest expenses you'll have, especially if you have a mortgage. -Excellent marketing is crucial. Post high-quality photos of your property so potential tenants get a great first-impression. You need to make sure your property is highly attractive. -Setting the correct rent price can be difficult, but talk with local Property Managers and agents and get their thoughts. This rental property is now officially out in the world and online! Let's get it rented! -Tyler I made a HUGE mistake. And I found out the hard way. In 2016, I blindly hired a property management company without vetting them at all. Never really spoke with them, definitely didn’t interview them, barely met them. And that was the downfall of My First Property. Fool me once...well, you know the saying.  So, prior to closing on My Second Property, I already had a new property management company lined up to take over. How? I got multiple property management company leads, interviewed them, and analyzed each one of them. This process of vetting IS CRITICAL to the health of your investment. Please, please, please, learn from my mistakes and hire the right company to manage your assets. Read all about my tips here: “How to Hire a Property Manager” My other strategy? I have two different companies managing my two properties at the same time (one to take over and manage the cleanup/sale of My First Property and one to manage My Second Property). This allows me to further vet each company and will aid in determining the best long-term fit for my management needs. Now, on to the terms of the property management company taking over My Second Property: -$895 New Lease Fee (i.e. I’ll pay $895 from my first month’s rent check) -I'll pay 9% of monthly gross rent (i.e. if my monthly rent is $1,000 – they get $90) -Professional listing photos -Pre-Move In Checklist, walkthrough, videos, and pictures -Rent directly pulled from Tenant’s checking account (reduces late rent!) -Specific tenant screening criteria Takeaways -Great property management is critical to owning a cash-flowing property -You must thoroughly vet the property management company you want to work with. Interview multiple companies and truly analyze each one. -Be sure to compare the specific terms of each property management company. How much do they take in monthly fees? What do they charge for a maintenance request? It's very important to know all expenses. Will this be the best property management company in the world? Maybe. Maybe not. But, I learned from my mistakes, did proper due diligence this time around, and interviewed multiple companies. Honestly, only time will tell if this is the best company for me. Let’s see how this plays out! -Tyler Looking at this whole journey of acquiring My Second Property, here's the simplified summary of it all: 1. Built connections in Indianapolis that would assist in finding future deals 2. Got pre-approved for financing 3. Started funneling in leads 4. Got a couple intriguing property leads from a turnkey company. Wasn't completely sold on them. 5. Decided to open up and look at other lead sources and reached out to an agent 6. Got a VERY intriguing lead that best fit my investing criteria 7. Got the property under contract after negotiating the sale price to my max budget 8. After reviewing the inspection report, negotiated the sale price down to $86,000 And, now we're here. All systems are a GO. We're on the home stretch.  My lender asks me for a few more things: -Complete a Credit Card Authorization form - to pay for the appraisal -Provide contact info for my insurance agent -Send over January and February checking account statements -Send over my last two pay stubs, my 2017 W2s, and information on my work history A couple days prior to the closing date (3/14), I receive the settlement statement from the Title company. The settlement statement is basically a rundown of exactly what I owe to the seller...it includes all the various fees and expenses. Total money out of my pocket for this deal? $22,435.66 And the final step? I had a mobile notary meet me at my office to sign the 111 page closing documents. All in all, the signing took about 30 minutes as I reviewed every document (read everything!!) and followed the direction of the notary. Man...my signature is seriously just a scribble now hahah! And with that, I closed on My Second Property. I'm excited for the future! After living through the ups and downs of My First Property, I learned a TON through first-hand experiences. Now with an adjusted strategy, I can't wait to see how this investment plays out. Next up: let's get this thing rented! -Tyler I'm officially in unknown territory. I've got a property under contract for $87,000 that was found by my agent. Yes, I've seen photos and videos of the place, but I honestly have no idea if it requires renovation or repairs. No worries! This is why the 15 day inspection period exists! Thankfully, I have a rockstar agent to guide me. My immediate action items: 1. Earnest Money - overnight a check for $1,000 to the selling agent ASAP. There's a three day deadline. 2. Inspection - I have 15 days to complete the inspection and an additional 10 days after that if needed. 3. Insurance - I must provide proof of insurance ASAP. 4. I must sign the Seller's Lead Based Paint disclosures. Couple other things: 1. My agent sent necessary paperwork to my lender to begin the application and financing side of things. 2. The tenant has now decided to leave. So, I will have a vacant property by the time I close. Which means, I'll need to have my property management begin marketing the property as soon as possible. One one hand, it sucks I won't have income coming in immediately, but on the other hand I can now screen and place my own tenant. Taking care of the Earnest Money, getting an insurance policy, and signing the Lead Based Paint disclosures were a piece of cake. Now, onto the INSPECTION. I initially tried to setup an inspection with the national company HouseMaster, but their earliest appointment time didn't work for me. So, I turned to one of my connections I met online and got a referral! Thanks to my first real estate mentor ever, Morgan! My inspection cost $310 based on square footage and all I had to provide was the property address and the listing agent's contact info. So what did the inspection uncover? -I should add a switch for the whole house fan. Right now, it's operated at the breaker box.  -There is unsecured wiring in the furnace room  -The kitchen and bathroom outlets are not GFCI protected -One window in the garage is broken -Plumbing was redone recently, but there are two mysteriously cut pipes in the crawl space.  -There's sign of a little mold in the crawl space. -The bathroom exhaust fan should vent to the exterior of home. It currently runs to the attic.  -The boiler heater is at end of its life cycle All in all, nothing too alarming! Knowing the boiler is toward the end of its life cycle isn't the greatest news, because that would be a major expense. I might need to hire a plumber to investigate the pipes in the crawlspace. And I should have an expert evaluate the mold in the crawl space. But, everything is pretty manageable. Because this is an "As-Is" transaction (the seller is unwilling to perform any repairs), I asked for a $1,000 reduction in asking price. I didn't want to rock the boat too much and lose the deal, since the inspection came back pretty clean. But, I did want a little cushion in case I have to repair the boiler in the near future. The seller immediately accepted my inspection response, which I kinda expected. They wouldn't kill the deal over $1,000 would they?? So, with the inspection complete, I really know the condition of the property. I'm all in...and I got it for under my maximum budget! Let's review this investment: Price: $86,000 Rent: $1,000 Beds: 2 Baths: 1 Square footage: 1,400 Built: 1950 Brick Ranch Two Car Garage Bonus sun room and full laundry room (could be converted to a 3rd bedroom) Full steam ahead! I'm Jumping In! Let's close! Takeaways -As an out of state investor, I 100% recommend you get an inspection on your property. That is a MUST for me to really understand the condition of the property. Trust the professionals! -Tyler With three great investment properties within reach, the biggest questions are: 1. Do I go after Leads #1 or #2 which are freshly rehabbed properties from a turnkey company? OR... 2. Do I go after Lead #3 which was found by my agent? First, let's take a closer look at each property: LEAD #1 Price: $84,900 Built: 1967 Beds: 4 Baths: 3 Square Feet: 1,360 Newly rehabbed RENT: $950 LEAD #2 Price: $82,900 Built: 1946 Beds: 3 Baths: 2 Square Feet: 1,134 Newly rehabbed RENT: $925 LEAD #3 Listed: $95,000 (negotiable because it's on the MLS) Built: 1950 Beds: 2 Baths: 1 Square Feet: 1,430 Not rehabbed RENT: $1,000 Soooo...what am I thinking? All properties meet my acquisition budget (under $100K), all properties meet the 1% rule (they each bring in at least 1% of the acquisition price in rent), and they're all brick ranches (I like brick in the Indianapolis weather). Ultimately, my decision came down to buying in the best neighborhood. And that = LEAD #3. Lead #3 also has the newest roof (which would be a large capital expense in the future), it brings in the most rental income, and it has the best chance of appreciation (being in the best neighborhood). On top of that...it's a wildcard...with 1,400+ square feet, there's enough room to add a 3rd bedroom if I decide to put a little money into it. This would greatly force appreciation. So, LEAD #3 it is! Now, on to my FIRST EVER offer and negotiation. If you remember, I bought My First Property through a turnkey company so there was no real negotiation or offer. I basically just said..."I'LL TAKE IT" and closed. Running numbers again, I'll tell you right now, the maximum price I could offer for Lead #3 was $87,000. It's important to know your max price before heading into a negotiation. Then, stay strict to your maximum and don't go over! Don't get emotionally tied to the investment. It's all about the numbers! Now...I get it...my maximum price of $87,000 is a solid $20,000 under their initial asking price of $107,000. Not the best offer...and I probably have a slim chance of even engaging the seller. But, they recently dropped the price to $95,000, so maybe I have a chance?? There are two basic negotiation tactics to understand when submitting an offer: 1. Submit your highest/best immediately, hope the seller accepts, and be happy with the ROI. 2. Submit under your highest and best, and try to negotiate the best ROI possible. For this property, I knew I wanted to give my offer a fighting chance, but I also wanted to give myself a little wiggle room to go up. I offered $86,000. And being pretty naive to all of this, I actually felt pretty confident with that. Other terms I included: 30 day close and 15 day inspection (with an additional 10 days of discovery). Surprisingly. They countered at $87,900. Wow, we're close here. They came down A LOT more than I expected. So I went straight to my highest and best at $87,000, fully confident we'd come to an agreement. Drum roll please....DONE.  They accepted at $87,000. A few electronic signatures here, a few electronic initials there, and we've got a deal! WOW...now it's real. And...crap...now I'm really Jumping Into unknown territory. Financing, an appraisal, an inspection...I've never done this before... Takeaways -Really know your numbers going into the negotiation phase. You have to understand what your max price will be before submitting an offer. -There are a couple negotiation strategies to consider: Offer your highest and max up front, or offer lower and work your way up. -Tyler "You da one that I dream about all day ay ay. You da one that I think about always..." Sorry, that Rihanna song just jumped into my head while writing the title of this post. ANYWAYS. Back to real estate. After receiving a couple promising property leads (Lead #1 and Lead #2), I didn't stop there, pick one, and plop down my money. Nope. Not that fast. While the numbers on paper for Leads #1 and #2 checked off most of my investing criteria boxes ($75k to $100k acquisition, bring in at least 1% rent at $900+), I honestly WASN'T 100% sold on the neighborhoods they were in. Remember, a huge goal of getting My Second Property, was to jump into a better neighborhood and attract a better tenant class. So, keeping my options open and casting a wider net for leads, I reached out to an agent I met briefly last year in Indianapolis. We'd connected online and I squeezed a quick little meeting in with her right before flying home to California. Naturally, we met at a Starbucks (I don't drink coffee...haha!). She immediately set me up with MLS alerts based on my criteria, which was amazingly helpful. And she also asked if I'd be willing to look outside of the typical 3 bed/1 or 2 bath houses that most investors were looking at. I told her I'd be flexible in house layout criteria (which later proved to be key), but I wouldn't compromise on my investment criteria. BOOM. Within 12 hours she sent me a lead. LEAD #3 Email from my Realtor: I just had one that popped up this morning that looked interesting in Washington Township - west side. I see now it's a 2/1, but it's actually quite a big 2/1 at 1400 sq ft. Tenants are already in place, but the listing doesn't say what they're currently paying. Rental comps are in the $1100-$1200 range. They actually just dropped the price on it this morning as well. I used to live just north of here - pretty decent area. I would say B class.

FIRST IMPRESSIONS OF LEAD #3: Holy crap. That wood paneling is UGLY. It's only a 2 bed/1 bath...not thrilled...will there be much rental demand for it?? At least it's got good square footage (1,400) and a 2 car garage with wrap-around driveway. Rental comps are actually higher ($1,100-$1,200) than my target and the property is listed at $95,000 which is under my budget. The seller also just reduced it from $107,000, which could mean they are super motivated to sell. You know what time it is now? Time to dig into the numbers and do some major research! Luckily, within a couple hours, my agent confirmed the tenants are paying $1,000 per month and they're on a month-to-month lease. Confirming the actual rent is HUGE, because estimating rent range can be difficult and it's such a critical number in calculating cash flow. $1k in rent is a little less than the initial estimate of $1,100-$1,200, but I can't complain, it fits my criteria and it's confirmed. After some quick calculations, the numbers look good! I'm VERY VERY interested. But, of course, I've got a few more questions. After all, this is the first property I've ever looked at without the help of a turnkey company. Venturing down this path of buying on my own, is completely unknown territory. I ask my agent a ton of questions: 1. How old is the roof? - Just over 1 year old. Roof and gutters replaced August 2016. 2. How old is the furnace? - It's a boiler. Great working condition. Age unknown. 3. Hold old is the water heater? - 3 years old. 4. Is it currently under a property management company? - It's self-managed by owner. 5. How long has the tenant been living there? - The tenants moved in 2014. 6. Can you send any more photos and videos? - Yes, but exact date to get into the property is unknown with tenants living there. Lesson #1: Your agent and the selling agent won't be able to answer every question right off the bat. Many infrastructure questions will most likely have to be answered by a professional inspector.

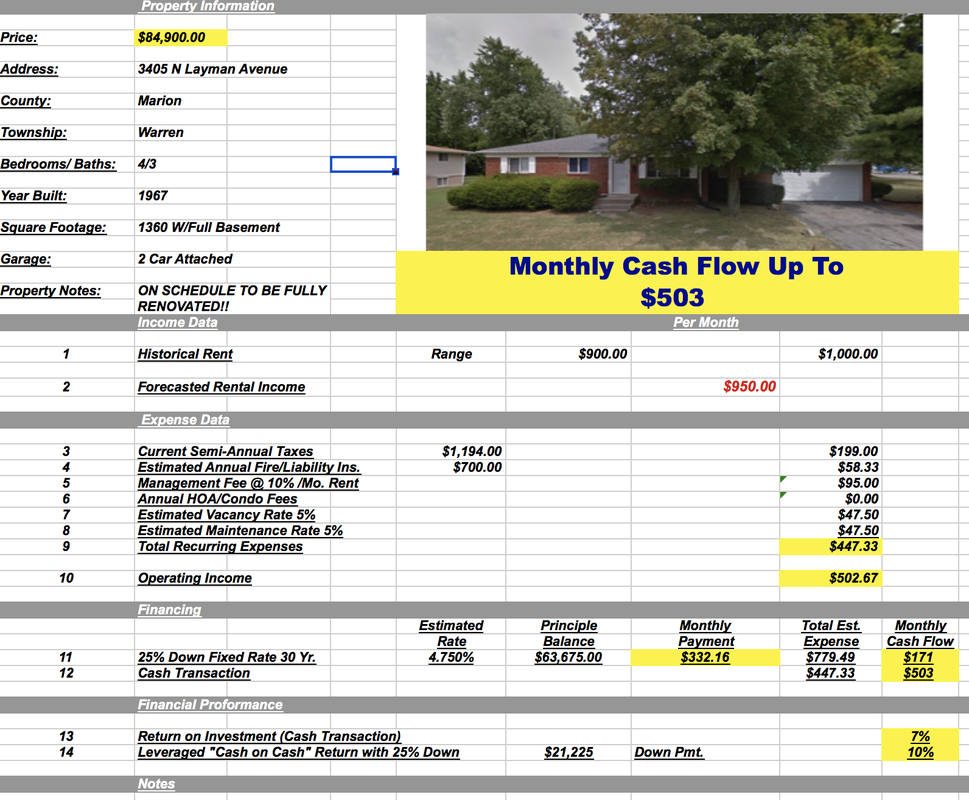

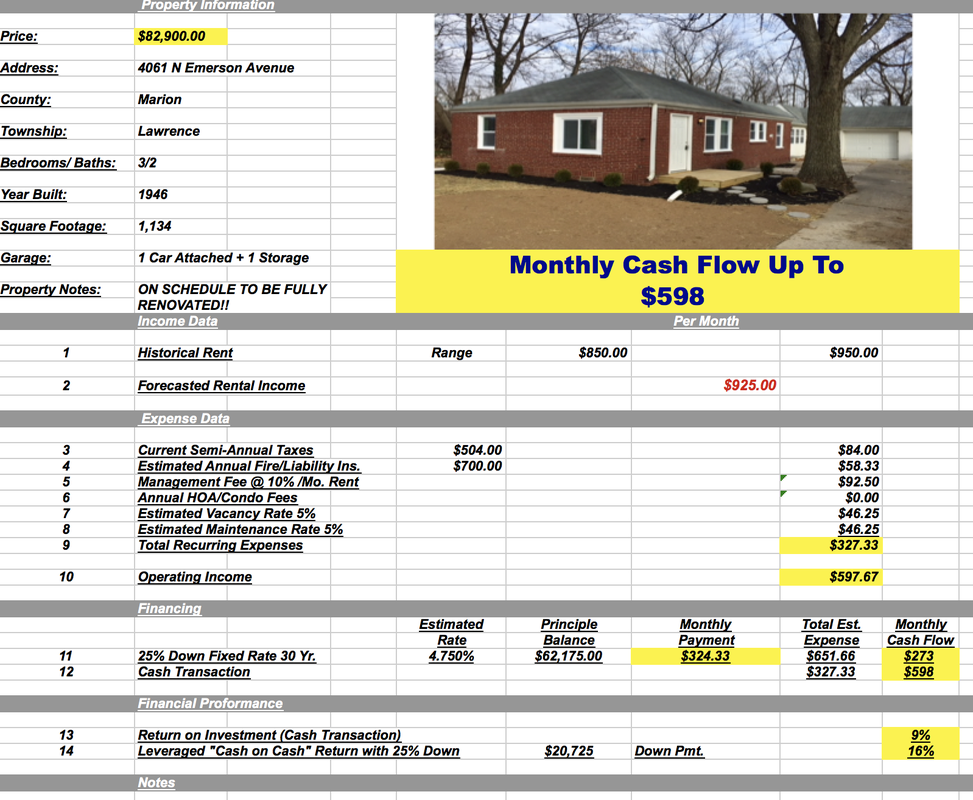

My agent coordinates a time to check out the property, then sends over photos, videos, and shoots me a note: All and all, nice property. The only thing I wasn’t a fan of is that it doesn’t have central air, but the list agent said the window unit does keep the whole house cool. Typically, though, that’s going to keep your rent lower than another unit with A/C. It’s on a broiler for heat as well, which I think might be better than having a furnace - probably not as energy efficient though. I don’t love that it doesn’t have a paved driveway either, but the gravel is pretty compact and if a tenant would need to shovel they shouldn’t have too much difficultly doing so. Property has been well maintained - as I mentioned new roof and gutters 2016, and the electrical box was updated in 2014. Flooring looks in good shape, and most of the walls are paneled, so not a lot of upkeep there. Also noticed that there was no dishwasher - again, typically something that is provided at this price point along with the A/C. Alright...so a couple little curveballs...no central AC and no dishwasher...but nothing horrible. Just a couple more questions for my agent: 1. What repairs do you think are needed? Fresh paint? New carpet? Garage windows? Anything big? - Depends on if the tenant stays or not. I would probably repaint any areas that aren't paneled and clean the carpet. It looked in pretty decent condition. Would repair the garage windows as well. 2. Any idea why they're selling? - It's the list agent's mom's property. It's the only rental property she owns, and probably sees it as a good time to sell. OK. NOW IT'S REALLY DECISION TIME. Work with a new turnkey company and go after Lead #1 or #2, which are both freshly rehabbed, and would probably be an easier transaction. Or, take matters into my own hands and go after Lead #3, which is in a better neighborhood, and would be a venture down an unknown road? -Tyler Going into the search for My Second Property, my knowledge base, experience, and connections have all immensely improved over the past year. With that, my investment criteria and strategy also shifted. Key strategy differences in my current search: 1. I'm financing this next property as opposed to paying all cash. This requires getting a mortgage, which I've already been approved for, and allows me to purchase a higher priced property with less money out of pocket. 2. I'm now targeting a property in the $75,000 - $100,000 price range that rents for $1,000/month. If you remember, My First Property was purchased for $37,000. A higher priced property will get me in a better neighborhood, should have better tenants, have less repairs, and a higher rate of appreciation.  I also now understand, when it comes to real estate investing, "the more risk, the more reward" is a valid expression. With me targeting a higher class neighborhood, I'm expecting my ROI to fall, but it should be a safer play with a stronger tenant and long-term returns. For example: I was getting a 14% ROI on My First Property with little stability, but now I'm estimating between 7%-10% on My Second Property with more stability. So, my first phone call to find property #2 was to an individual I connected with online. We had a couple great phone conversations and then eventually met in person in Indianapolis (he met me on a Saturday morning at 8:30am...LOVE the dude!). His company follows the Turnkey model: they purchase properties, renovate them, sell them to investors, and manage them. The biggest difference between his company and the one I worked with previously: their properties are in the $75,000 - $100,000 range. They DON'T TOUCH C-Class low-end inventory...something I'm very happy about. After a few weeks of back and forth conversation, and patiently (not really...) waiting to see their inventory, I was sent a package of 5 houses. Below are two that stood out to me. LEAD #1 This property is vacant and scheduled to be fully renovated.  *This data was provided by the investing company. These are not my calculations* FIRST IMPRESSION OF LEAD #1: I like the curb appeal, brick exterior (great in the Indy weather), and 2 car garage. It's a large home with 4 bedrooms and 3 bathrooms, but having 3 bathrooms actually scares me a little...that means three times the toilets and plumbing to deal with. The acquisition price ($84,900) to rent ($950) ratio is great and exactly what I'm looking for from an investment standpoint. LEAD #2 This property is vacant and scheduled to be fully renovated.  *This data was provided by the investing company. These are not my calculations* FIRST IMPRESSION OF LEAD #2: I also like the curb appeal, brick exterior, and garage. It has less square footage with 3 bedrooms and 2 bathrooms. But, as I mentioned before, I don't mind the smaller floorpan and one less bathroom. However, this house is about 20 years older than Lead #1. The acquisition price ($82,900) to rent ($925) ratio is great, but I would prefer rent a little closer to $1,000. So, I got right to work and dug into the numbers a little more! By now, analyzing properties has become a lot easier, and I now have processes and a strong system in place. I look back at analyzing My First Property before purchasing it, and I was quite foolish. I really did JUMP IN rather blindly. But, that's beside the point now. Thankfully, I've learned a ton and now initially look at these core questions: -Does it meet the 1% Rule? -Can I get it for under-market value? -Is it in a good neighborhood? -How are the schools? -Is it in a flood zone? -What's the zip code like? I then calculate all expenses and income. How? Well, you're in luck! Check out my post on How to Analyze Property. After a quick analysis, LEAD #2 came out on top! So I asked a few more questions (with answers in red) and got additional photos. 1. How old is the roof? - NOT SURE EXACTLY. OUR ROOFER ESTIMATED 8-10 YEARS OLD. 2. How old is the furnace? - INSTALLED NEW FURNACE. 3. How old is the water heater? - INSTALLED NEW WATER HEATER. 4. What condition are the windows in? - WE INSTALLED NEW VINYL WINDOWS AND SLIDER.

The place looks nice!!! The numbers look great!! I'm excited! I'm pumped! Could this be my next investment??? Am I one step closer to Financial Independence?? Ok...now I'm a little nervous...I thought it'd be easier to pull the trigger on My Second Property. I've got more experience under my belt...right? Decisions...decisions.... Takeaways -Investment strategies change. A year ago, the properties I was targeting were completely different from the ones I am now looking at. That's the beauty of experience. You learn and grow. -I thought it would be a lot easier pulling the trigger on My Second Property. Yes, it's no longer "my first rodeo" but there's still challenges, questions, and doubts that creep into your brain. -Tyler The first major difference between purchasing My First Property and purchasing My Second Property, is the financing strategy I'm using. While I paid ALL CASH for My First Property, I don't have the reserves to purchase this next investment outright. But, I'm fine with that. I really have no desire to buy it cash even if I could. Why? Through my experience purchasing one property all cash, I realized the amazing power of leverage. Yes, cash flow is negatively affected with a mortgage, but your dollars can go much further, you can scale much faster, and your cash-on-cash return can be larger. Check out my post on the various Pros and Cons of having a mortgage vs. paying all cash HERE.  So, the adventure to find money began. Luckily, as I mentioned in my previous post, I met some great connections in Indy. Through the jam-packed weekend I connected with a lender who is now a crucial, crucial component of acquiring My Second Property. The process of getting a mortgage was a little intimidating at first...I'd never gotten one before! But, looking back, it was smooth overall. A little laborious, a lot of documents had to be tracked down, but again, very smooth. So what was the process like? Step 1 Fill out an Online Mortgage Application. This required basic contact information as well as: -Loan information (how much are you asking for?) -Detailed personal information -Employment and Income information -Assets and Liability information -Declarations -Consent and Confirmation This all took about 15-20 minutes to compile and complete. Step 2 After submitting the online application, I got in touch with my lender and he required a few additional documents: -Last two paystubs -The past two years W2s -The past two years tax returns -Last two bank statements for all accounts -Copy of my driver's license He also set up a BOX account (cloud storage) so I could upload everything for his team to access instead of emailing everything over. Step 3 This step was a simple waiting game as the lender had to assess my qualifications. Within a day, I was pre-approved! I'm going to assume it helped that I'm targeting a property in the $100,000 range...and not a house in the Bay Area for $700,000. Key Information when applying for a mortgage -Lenders won't give out loans to financially risky individuals. A good credit score, a steady paying W2 job (being self-employed makes you a little more risky to lenders), and having a sizable cash reserve will help your case for a mortgage. Make sure these are in tip-top shape before looking for a loan. -If you plan to purchase a distressed property...one that needs a lot of rehab work...don't assume you can get it financed. Lenders won't provide financing for risky assets. -Keep your files and documents organized! If you plan to build a large real estate portfolio with the help of bank financing, this won't be the only time you'll be asked for a W2 from two years ago or your tax return from last year. -Mortgage rates change daily, so if you're getting 4.5% one day, it could easily jump to 4.75% the next day. Before offering on a property, always ask your lender for the most up-to-date interest rate so you can accurately analyze it.  And with that, I'm ready to look for my next investment! I've got a pre-approval letter in hand, a $100,000 budget, specific investment criteria in my head, and a new sense of excitement. I'm jumping in to property #2. LET'S DO THIS! -Tyler |

Browse Topics

All

|

Investing |

Jump In |

|